Most people think these three account types are interchangeable.

They are not.

They are designed for three distinct jobs within a healthy financial system.

Using the wrong account for the wrong purpose creates overspending, inconsistent saving, and financial stress — even when income is sufficient.

Instead of asking which account is best, the better question is:

What role should each account play?

Once each account has a defined responsibility, money management becomes dramatically easier.

You can see a practical, real-world structure example here:

https://thedigitalincome.com/comprehensive-review-of-wealthfronts-cash-account/

The Three-Layer Money System

Think of your finances as a workflow, not a container.

| Account Type | Role | Behavior Outcome |

|---|---|---|

| Checking | Movement | Spending |

| Savings | Storage | Holding |

| Cash Management | Separation | Consistency |

Each solves a different behavioral problem.

When combined correctly, budgeting becomes almost automatic.

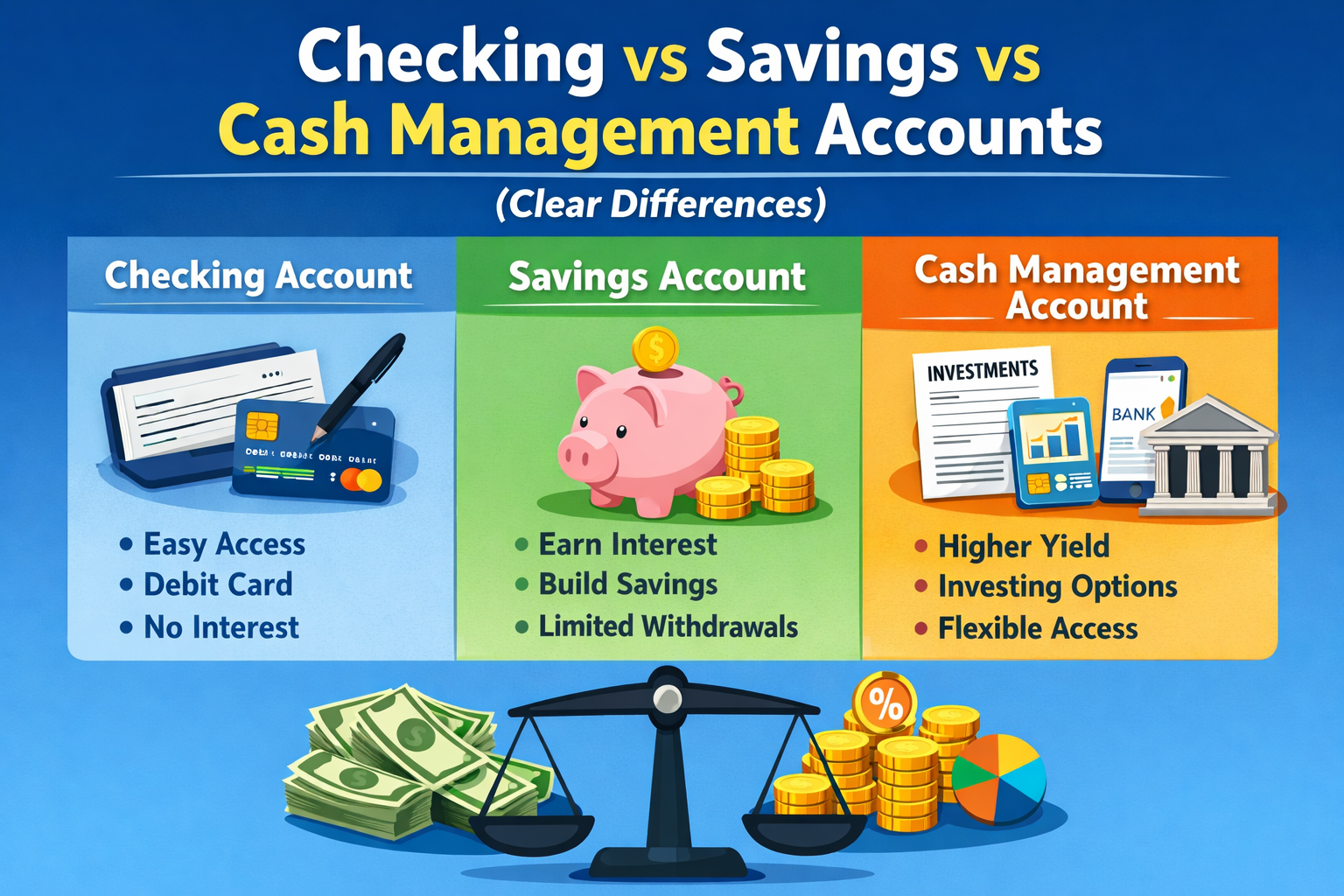

Checking Account — The Transaction Engine

Purpose: movement

Checking accounts exist to handle money in motion.

They are optimized for speed, access, and convenience — not preservation.

Best Uses

-

Paying bills

-

Debit card purchases

-

Subscriptions

-

Everyday spending

-

Incoming paychecks

This is your operational wallet.

Strength

Maximum convenience

Weakness

Maximum visibility

Humans spend what they constantly see.

Keeping large balances in checking increases spending frequency without conscious awareness.

Checking accounts are designed for activity, which makes them poor storage locations.

Savings Account — The Holding Container

Purpose: storage

Savings accounts exist to hold money that shouldn’t be spent immediately but still needs to be accessible.

They introduce a small friction step between intention and action.

Best Uses

-

Short-term goals

-

Small reserves

-

Planned purchases

-

Temporary holding

Strength

Stable and predictable

Weakness

Requires manual discipline

Most savings failures happen here — not because of low interest, but because moving money requires repeated decisions.

You must constantly decide to save.

Over time, decision fatigue reduces consistency.

Cash Management Account — The Separation Layer

Purpose: automation and allocation

Cash management accounts are designed to solve a behavioral problem:

People don’t struggle with knowing they should save —

They struggle with doing it repeatedly.

Instead of relying on manual transfers, the system automatically allocates funds.

Typically Combines

-

Savings-level interest

-

Automatic transfers

-

Categorized reserves

-

Distance from spending

You can see a practical usage example here:

https://thedigitalincome.com/comprehensive-review-of-wealthfronts-cash-account/

Strength

Reduces reliance on discipline

Weakness

Not ideal for daily spending

It intentionally sits between checking and investing.

Why This Matters More Than Budgeting

Budgeting apps try to control behavior after money is visible.

Account structure controls behavior before spending happens.

| Method | Difficulty |

|---|---|

| Budget tracking | Requires constant attention |

| Account separation | Works automatically |

Structure beats willpower.

How Each Account Influences Behavior

Checking Encourages Spending

Immediate access = frequent use

Savings Encourages Decisions

Manual transfers = inconsistent habits

Cash Accounts Encourage Consistency

Automatic allocation = stable growth

Money location changes behavior more than financial knowledge.

The Ideal Financial Flow

A simple but effective system:

Income → Checking (operations)

Excess → Cash account (protection)

Surplus → Investments (growth)

Each dollar receives a job immediately after arriving.

This removes the common question:

“Can I afford this?”

Because the spending account already contains the answer.

Real-Life Example

Instead of holding $6,000 in checking:

-

$1,200 stays in checking (monthly spending)

-

$3,800 moves automatically to cash reserves

-

$1,000 goes toward long-term investing

Same income.

Different structure.

Completely different financial outcome.

Why Most People Struggle Without This

Without separation:

-

Spending and saving compete

-

Emergencies disrupt plans

-

Investing feels risky

With separation:

-

Spending becomes predictable

-

Emergencies stay contained

-

Investing becomes consistent

The accounts don’t just store money — they create decision boundaries.

Final Takeaway

These accounts are not competitors.

They are components of a complete financial system.

Checking manages activity.

Savings stores funds temporarily.

Cash management automates protection.

When used together, they reduce financial stress more effectively than tracking expenses alone.

See a working example here:

https://thedigitalincome.com/comprehensive-review-of-wealthfronts-cash-account/

Leave a Reply